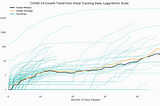

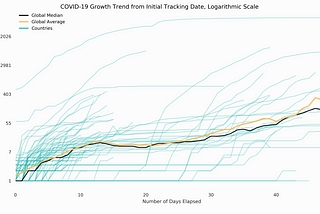

Sebastian QuinteroinTowards Data ScienceEstimating the Number of Future Coronavirus Cases in the United StatesWith the CDC and US authorities scrambling to get enough coronavirus tests ready for the public, it would be helpful if we could estimate…Mar 11, 20209Mar 11, 20209

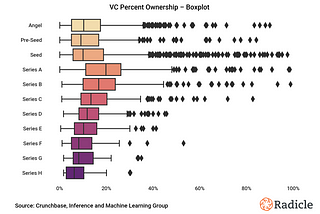

Sebastian QuinteroinJournal of Empirical EntrepreneurshipDemystifying Startup Equity with Data ScienceWhat percentage of ownership do investors acquire at each financing stage?Jun 10, 20192Jun 10, 20192

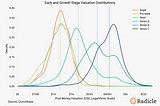

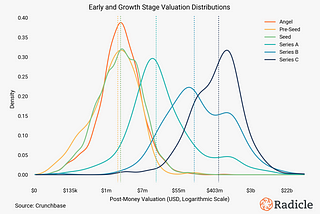

Sebastian QuinteroinJournal of Empirical EntrepreneurshipPredicting a Startup Valuation with Data ScienceThe following is a condensed and slightly modified version of a Radicle working paper on the startup economy in which we explore…Jan 30, 20199Jan 30, 20199

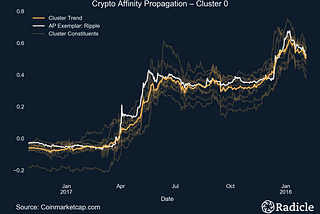

Sebastian QuinteroinTowards Data ScienceClustering Cryptocurrencies with Affinity PropagationTo better understand coin correlations we deployed an Affinity Propagation algorithm and found three distinct clusters of crypto assets, at…Apr 9, 20183Apr 9, 20183

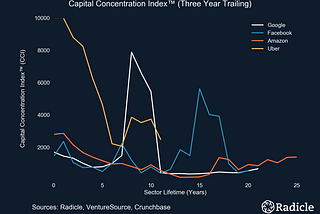

Sebastian QuinteroinJournal of Empirical EntrepreneurshipIntroducing the Capital Concentration Index™A measure of startup competition.Dec 20, 2017Dec 20, 2017

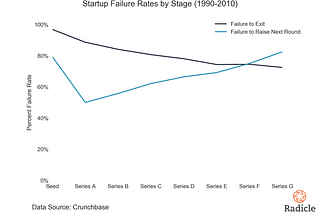

Sebastian QuinteroinJournal of Empirical EntrepreneurshipDissecting startup failure rates by stageA few weeks ago in an article titled “How much runway should you target between financing rounds?”, we discovered that the conventional…Nov 8, 20179Nov 8, 20179

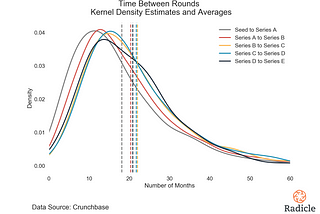

Sebastian QuinteroinJournal of Empirical EntrepreneurshipHow much runway should you target between financing rounds?Entrepreneurs have limited access to hard data that could help them make sound decisions when trying to build a successful new company…Oct 26, 20174Oct 26, 20174

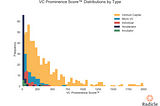

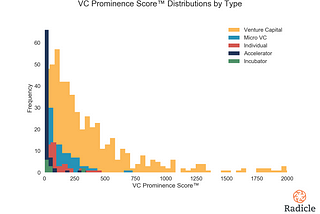

Sebastian QuinteroinJournal of Empirical EntrepreneurshipIntroducing the Investor Cluster Score™ — a measure of the signal produced by a startup’s…If you look at any TechCrunch article that announces the latest round of funding for the next promising startup, you’ll notice that the…Oct 13, 20171Oct 13, 20171